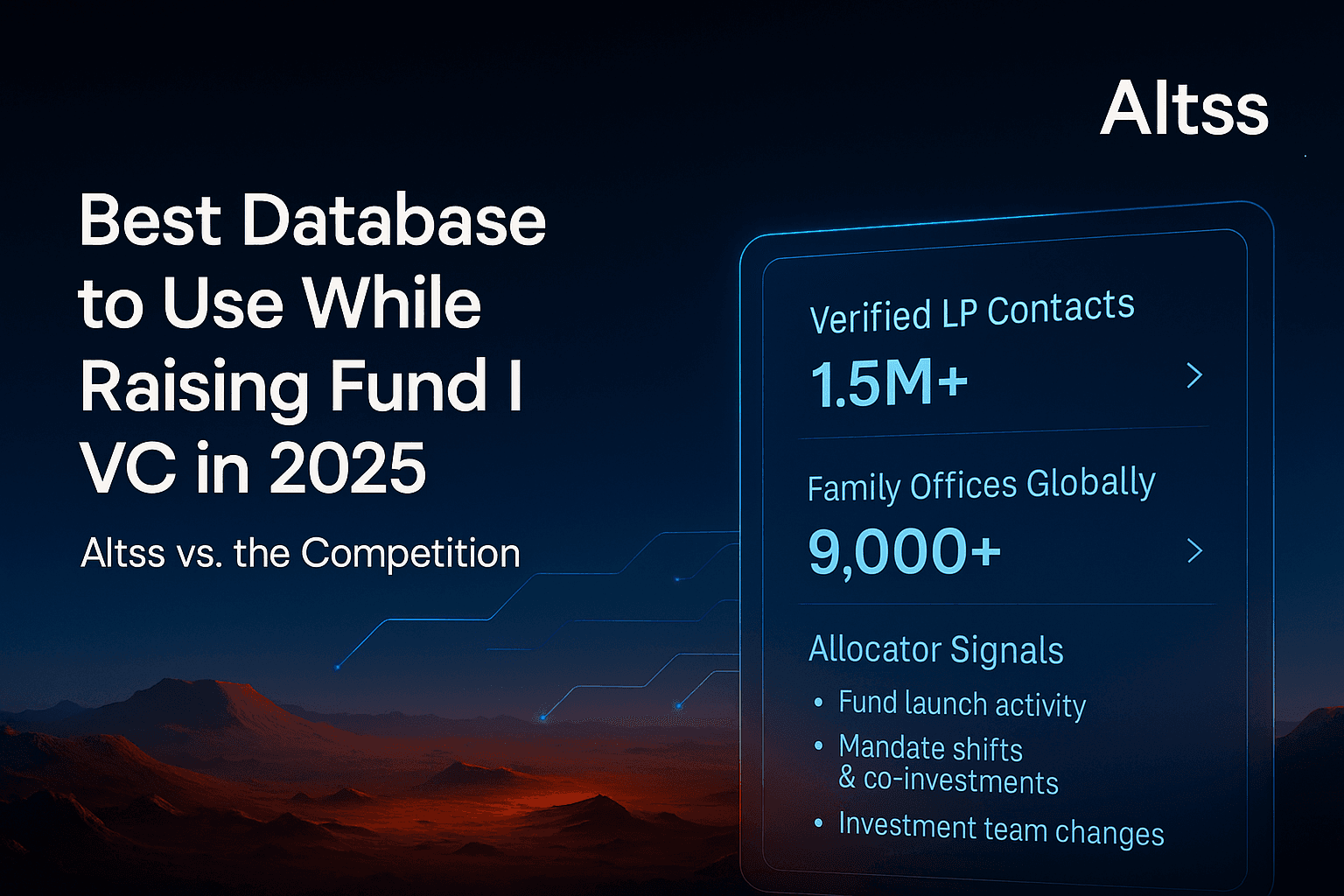

Best Database to Use While Raising Fund I VC in 2026: Altss vs. the Competition

Fund I venture managers need family office depth, continuously refreshed allocator signals, and personalization-ready data — not institutional directories built for Fund IV teams. Altss delivers 9,000+ verified family offices, OSINT-powered freshness on a sub-30-day update cycle, and decision-maker mapping that legacy platforms like Preqin, Dealroom, and Dakota cannot match for Fund I targeting. Pricing starts at $12,000/year for FO coverage, with Full LP coverage at $15,500/year.

The Fund I Reality: Why Traditional LP Lists Rarely Work

Fund I managers operate in a fundamentally different environment from established firms. They start with no long institutional track record, limited DPI or realizations, a smaller active network, limited internal IR capacity, higher scrutiny from allocators, and a need for personalization that feels authentic, not formulaic.

The friction is not fundraising difficulty itself. It is the mismatch between Fund I needs and legacy tools.

Most LP databases were built for firms raising Fund IV or later. They assume the user has a dedicated IR team, a decade of performance data, and relationships that can be supplemented by directory-style lookups. Fund I managers have none of that. They need intelligence that reveals not just who allocators are, but what they care about, how they invest, and whether they are actively looking at new managers right now.

In 2026, that gap has widened. LPs are more selective. Family offices now deploy over $1.2 trillion in alternative assets globally, per the latest Global Family Office Report. Private wealth intermediaries — RIAs, multifamily offices, and independent advisors — control an estimated $4.5 trillion in allocable private-market capital. Institutional LPs have slowed their pace of new manager onboarding. The average pension fund added just 2.3 new manager relationships in 2025, down from 4.1 in 2020.

The old approach — buying a list of 10,000 LP names and blasting emails — yields response rates below 0.5% for Fund I managers. The new approach requires targeting the right 50 to 100 allocators who are structurally aligned, thematically interested, and actively deploying.

The LP Database Landscape in 2026

The market for LP intelligence has fragmented. No single platform dominates because no single platform serves every use case. But for Fund I venture managers, the choice narrows to five primary options:

| Platform | Core Strength | Fund I Fit | Price Range |

|---|---|---|---|

| Altss | Family office depth, OSINT signals, sub-30-day refresh | Excellent | $12k–$15.5k/yr |

| Preqin | Institutional LP coverage, benchmark data | Moderate | $15k–$30k+/yr |

| Dealroom | Company and deal data, European focus | Weak | $10k–$25k/yr |

| Dakota | Institutional LP relationships, CRM integration | Moderate | $20k–$50k+/yr |

| FINTRX | Family office and RIA coverage | Good | $10k–$20k/yr |

| IHS Markit (now S&P) | Institutional LP data, insurance assets | Weak | $25k+/yr |

Each platform has its lane. But the Fund I use case demands specific capabilities that most platforms underinvest in.

What Fund I Managers Actually Need

Fund I fundraising is a targeting problem disguised as a relationship problem. The relationship part comes later. First, you must find the allocators who are:

Thematically aligned. A climate tech fund should not pitch a healthcare-only endowment. A fintech fund should not waste time with an LP that only does buyout. Yet most LP databases offer only high-level sector tags — "VC," "growth," "buyout" — without mapping thesis-level alignment.

Structurally flexible. Many institutional LPs have hard caps on first-time funds, vintage concentration limits, or mandates that require $100M+ minimum commitments. Fund I managers typically raise $25M–$75M. They need LPs that do not have minimums that exclude them.

Actively deploying. An allocator that last committed to a VC fund in 2022 is unlikely to be the right target in 2026. Fund I managers need to know who is in the market now, not who was active three years ago.

Reachable. This is the hardest part. Most LP databases have generic contact information — a main office number, a general email, a LinkedIn profile that may or may not be monitored. Fund I managers need decision-maker-level contacts with verified email addresses and direct phone numbers.

Personalizable. Fund I managers cannot send generic pitch decks. Every outreach must demonstrate specific knowledge of the allocator's portfolio, thesis, and preferences. That requires data — recent investments, stated interests, conference appearances, published research, and social media activity.

Legacy platforms like Preqin and Dakota provide some of this data, but they are optimized for institutional LPs with large IR teams. They assume the user has the time and resources to manually filter, verify, and enrich the data. Fund I managers do not.

Altss: Built for the Fund I Problem

Altss was designed specifically for the Fund I use case. Its core differentiators are not features but data architecture choices that matter most to emerging managers.

Family office depth. Altss tracks over 9,000 family offices globally. That is not a count of registered entities — it is a count of verified allocators with confirmed assets under management, investment mandates, and decision-maker contacts. For context, Preqin tracks approximately 3,500 family offices. FINTRX tracks about 4,200. Altss has invested heavily in OSINT-based verification — using public records, regulatory filings, news monitoring, and social media analysis to confirm that each family office is actively investing.

Sub-30-day update cycle. LP data decays fast. Allocators change jobs. Family offices shift strategies. Contact information becomes stale. Altss updates its entire dataset on a sub-30-day cycle. That means when a Fund I manager searches for "climate tech family offices in Europe," they see allocators that were active within the last month, not the last year.

Decision-maker mapping. Altss does not just list organizations. It maps the decision-making structure of each allocator — who the CIO is, who the investment committee members are, who the gatekeepers are, and how decisions actually get made. For family offices, that often means identifying the family member or external CIO who controls allocations. For institutional LPs, it means mapping the analyst, director, and CIO roles.

OSINT-powered signals. Altss ingests publicly available data from thousands of sources — SEC filings, 13F and 13D forms, Form Ds, news articles, conference agendas, podcast appearances, social media posts, and regulatory filings — to generate signals about allocator activity. If a family office CIO speaks at a climate tech conference, Altss flags it. If an endowment publishes a new investment policy statement, Altss surfaces the changes. If an RIA files a new Form ADV with updated private-market allocation targets, Altss captures it.

Personalization-ready data. Every allocator record in Altss includes not just contact information but a structured profile of investment preferences, recent activity, and stated interests. Fund I managers can filter by sector, stage, geography, check size, and time since last commitment. They can also search by keywords — "first-time fund," "emerging manager," "diverse manager" — to find allocators with explicit mandates for Fund I.

Preqin: The Institutional Benchmark

Preqin remains the most widely used LP database in private markets. Its strengths are real: comprehensive coverage of institutional LPs, robust benchmark data, and a long track record of industry research. For Fund IV+ teams, Preqin is often sufficient.

But for Fund I managers, Preqin has three structural weaknesses.

Weak family office coverage. Preqin tracks approximately 3,500 family offices, but many of those entries are based on voluntary surveys or public filings that are months or years old. Altss has verified 9,000+ family offices through continuous OSINT methods, and its refresh cycle is significantly faster.

Static contact data. Preqin's contact data for family offices and smaller institutional LPs is often generic — a main phone number, a general email, or a LinkedIn profile that may not be monitored. Fund I managers need direct lines to decision-makers, not front-desk numbers.

No decision-maker mapping. Preqin lists organizations, not people. It does not map who makes investment decisions, who influences those decisions, or how the decision process works. For Fund I managers who need to personalize outreach, that is a critical gap.

Slow update cycle. Preqin updates its LP data quarterly or semi-annually. In a market where allocator activity changes weekly, that lag creates risk. A Fund I manager using Preqin might target an allocator that stopped investing in venture six months ago.

Preqin costs $15,000–$30,000+ per year depending on modules. For Fund I managers with limited budgets, that is a significant expense for data that does not fully address their needs.

Dealroom: The European Company Data Specialist

Dealroom is a strong platform for company and deal data, particularly in Europe. It excels at tracking startup ecosystems, funding rounds, and exit activity. But it is not built for LP intelligence.

Dealroom's LP coverage is thin. It lists allocators primarily as investors in rounds, not as independent entities with their own investment mandates, preferences, and contact information. Fund I managers cannot use Dealroom to build a targeted LP list, map decision-makers, or track allocator activity over time.

Dealroom is useful for one thing in the Fund I context: identifying which LPs have invested in companies similar to the fund's thesis. A Fund I manager focused on climate tech can use Dealroom to see which LPs have participated in climate tech rounds. But that is a starting point, not a complete solution.

Dealroom costs $10,000–$25,000 per year. For Fund I managers, it is a supplement to an LP database, not a replacement.

Dakota: The Institutional Relationship Manager

Dakota is the most established platform for institutional LP relationship management. It is used by large asset managers, pension funds, and endowments to track their LP relationships. Its CRM features are robust, and its data on institutional LPs is generally accurate.

But Dakota was built for large IR teams, not Fund I managers. Its pricing — $20,000–$50,000+ per year — is prohibitive for most emerging funds. Its data is focused on institutional LPs, not family offices or RIAs. And its contact data, while better than Preqin's, is still not optimized for the personalization that Fund I managers need.

Dakota's decision-maker mapping is limited. It lists contacts but does not always clarify who has decision-making authority. For Fund I managers who need to identify the right person at each allocator, that is a problem.

Dakota also has a slow update cycle. Its data refreshes quarterly, and some records are outdated by months or years.

FINTRX: The Family Office and RIA Specialist

FINTRX is the closest competitor to Altss in the family office space. It tracks approximately 4,200 family offices and 8,000 RIAs. Its data is generally accurate, and its pricing — $10,000–$20,000 per year — is accessible for Fund I managers.

But FINTRX has three weaknesses relative to Altss.

Smaller family office coverage. Altss tracks 9,000+ family offices, more than double FINTRX's count. That difference matters for Fund I managers who need to cast a wide net.

Slower update cycle. FINTRX updates its data quarterly. Altss updates on a sub-30-day cycle. In a market where allocator activity changes weekly, that speed advantage is significant.

Less decision-maker mapping. FINTRX provides contact information but does not systematically map decision-making structures. Altss profiles each allocator's investment committee, gatekeepers, and decision process.

No OSINT signals. FINTRX relies primarily on surveys and public filings. Altss ingests thousands of additional data sources — news, social media, conference agendas, regulatory filings — to generate signals about allocator activity.

IHS Markit (S&P): The Institutional Giant

IHS Markit, now part of S&P Global, provides institutional LP data primarily for insurance companies, pension funds, and sovereign wealth funds. Its coverage of those segments is strong. But for Fund I venture managers, it is a poor fit.

IHS Markit's family office coverage is minimal. Its contact data is generic. Its pricing — $25,000+ per year — is high. And its platform is designed for large institutional investors, not emerging managers.

The Data Quality Problem

All LP databases face the same fundamental challenge: data decays. Allocators change jobs. Family offices shift strategies. Contact information becomes stale. The question is not whether data decays but how quickly each platform detects and corrects decay.

Altss addresses this through its sub-30-day update cycle. Every allocator record is reviewed and refreshed at least once per month. If a contact changes jobs, Altss captures it within 30 days. If a family office stops investing in venture, Altss flags it within 30 days. If an RIA files a new Form ADV with updated allocation targets, Altss ingests it within 30 days.

Preqin, Dakota, and FINTRX update quarterly or semi-annually. That means their data can be three to six months old. For Fund I managers who need to know who is active right now, that lag is dangerous.

The cost of stale data is not just wasted outreach. It is damaged credibility. A Fund I manager who pitches an allocator that stopped investing in venture 18 months ago looks unprepared. A manager who emails a contact that left the firm six months ago looks sloppy. In a fundraising process where first impressions matter, data quality is a competitive advantage.

The Personalization Imperative

Fund I managers cannot send generic pitch decks. Every outreach must demonstrate specific knowledge of the allocator's portfolio, thesis, and preferences. That requires data — recent investments, stated interests, conference appearances, published research, and social media activity.

Altss provides this data natively. Every allocator record includes a structured profile of investment preferences, recent activity, and stated interests. Fund I managers can filter by sector, stage, geography, check size, and time since last commitment. They can also search by keywords — "first-time fund," "emerging manager," "diverse manager" — to find allocators with explicit mandates for Fund I.

Preqin and Dakota provide some of this data, but they do not structure it for personalization. A Fund I manager using Preqin must manually review each allocator's profile, read their website, and search for recent news. That is time-consuming and error-prone. Altss automates much of that work.

The OSINT Advantage

Altss is the only LP database built on OSINT — open-source intelligence. That means it ingests data from thousands of publicly available sources, not just voluntary surveys or paid data feeds.

The sources include:

SEC filings. 13F and 13D filings reveal what allocators are buying and selling. Form D filings reveal which funds they are investing in. Form ADV filings reveal RIA allocation targets and strategies.

Regulatory filings. State pension fund records, insurance company filings, and sovereign wealth fund disclosures provide detailed information about allocator activity.

News articles. Altss monitors thousands of news sources for mentions of allocator activity — new hires, strategy changes, fund commitments, and conference appearances.

Conference agendas. When allocators speak at conferences, they reveal their current interests and priorities. Altss captures that data.

Social media. LinkedIn, Twitter, and other platforms provide signals about allocator activity. Altss monitors these sources for job changes, content sharing, and engagement.

Podcast appearances. Allocators who appear on podcasts often discuss their investment philosophy, current focus areas, and deal criteria. Altss captures and structures that data.

Public records. Corporate registrations, property records, and tax filings provide additional context about allocator activity.

No other LP database uses this approach. Preqin relies primarily on surveys. Dakota relies on client-provided data. FINTRX relies on public filings and surveys. Altss's OSINT methodology gives it a data freshness and depth advantage that is particularly valuable for Fund I managers.

The Pricing Landscape

LP database pricing varies widely. For Fund I managers with limited budgets, cost is a significant factor.

| Platform | Annual Price | What You Get |

|---|---|---|

| Altss FO | $12,000 | 9,000+ family offices, sub-30-day refresh, decision-maker mapping, OSINT signals |

| Altss Full LP | $15,500 | All FO coverage plus 30,000+ institutional LPs, RIAs, and family offices |

| Preqin | $15,000–$30,000+ | Institutional LP data, benchmarks, quarterly updates |

| Dealroom | $10,000–$25,000 | Company and deal data, limited LP coverage |

| Dakota | $20,000–$50,000+ | Institutional LP CRM, quarterly updates |

| FINTRX | $10,000–$20,000 | 4,200 family offices, 8,000 RIAs, quarterly updates |

| IHS Markit | $25,000+ | Institutional LP data, limited family office coverage |

Altss's pricing is competitive for the value it delivers. At $12,000 per year for family office coverage, it is cheaper than Preqin or Dakota. At $15,500 per year for full LP coverage, it is cheaper than most institutional alternatives.

But price is not the only factor. The cost of missed opportunities — pitching the wrong allocators, using stale data, failing to personalize — far exceeds the cost of any database subscription.

How to Evaluate LP Databases for Fund I

Fund I managers should evaluate LP databases based on five criteria.

Coverage depth. How many allocators in the fund's target segment does the database cover? For Fund I venture managers, family office coverage is critical. Look for databases with 5,000+ verified family offices.

Data freshness. How often does the database refresh its data? Sub-30-day refresh is ideal. Quarterly refresh is too slow for Fund I fundraising.

Decision-maker mapping. Does the database list organizations or people? Does it clarify who makes investment decisions? Does it provide direct contact information for decision-makers?

Personalization data. Does the database provide structured data about allocator preferences, recent activity, and stated interests? Can you filter by sector, stage, geography, and check size?

OSINT signals. Does the database ingest publicly available data from multiple sources? Does it surface signals about allocator activity — new hires, strategy changes, conference appearances?

No single database scores perfectly on all five criteria. But Altss comes closest for Fund I managers.

Practical Advice for Fund I Managers

Based on our analysis, here is practical advice for Fund I managers evaluating LP databases.

Start with Altss. For Fund I venture managers, Altss is the best option. It provides the deepest family office coverage, the freshest data, and the most personalization-ready profiles. Its OSINT signals give you an edge in identifying active allocators. Its pricing is accessible for emerging funds.

Use Preqin as a supplement. If you have budget for a second database, Preqin provides institutional LP coverage that Altss does not fully replicate. Use Preqin for pension funds, endowments, and foundations. Use Altss for family offices, RIAs, and wealth intermediaries.

Skip Dealroom for LP targeting. Dealroom is excellent for company and deal data. It is not a substitute for an LP database. Use it for research, not targeting.

Consider FINTRX as a budget alternative. If Altss is out of budget, FINTRX is a reasonable alternative for family office coverage. But you will get fewer family offices and slower data refresh.

Avoid Dakota for Fund I. Dakota is built for large IR teams. Its pricing, data structure, and update cycle are not optimized for Fund I managers.

Invest in data enrichment. No database is perfect. Plan to spend 10–20 hours per month enriching and verifying your data. Cross-reference contacts on LinkedIn. Check allocator websites. Monitor news for activity signals.

Build a targeting framework. Before you start using any database, define your target allocator profile. What sectors, stages, geographies, and check sizes are you targeting? What types of allocators are most likely to invest in Fund I? Use the database to filter against that profile, not to explore randomly.

Track your outreach. Use a CRM to track every interaction with allocators. Note what you learned, what signals you observed, and what follow-up is needed. The database is a starting point, not an ending point.

The Future of LP Intelligence

The LP database market is evolving rapidly. Three trends will shape the next five years.

OSINT will become standard. As allocators leave more digital signals — through social media, conference appearances, regulatory filings, and news coverage — databases that ignore those signals will become obsolete. Altss is ahead of this trend, but competitors will catch up.

Decision-maker mapping will deepen. Databases will move beyond listing contacts to mapping decision-making structures. They will identify who has authority, who influences decisions, and how the process works. Altss already does this for family offices. Expect others to follow.

Personalization will become automated. Databases will not just provide data for personalization; they will generate personalized outreach templates based on allocator profiles. Altss is exploring this capability.

Real-time signals will emerge. As data freshness improves, databases will move from periodic updates to continuous refresh. Sub-30-day cycles will become sub-weekly. Weekly will become daily.

Pricing will compress. As competition increases, pricing will decline. Altss's pricing is already competitive. Expect Preqin and Dakota to face pressure to lower prices or improve value.

Conclusion

Fund I venture managers face a unique challenge. They need to find a small number of thematically aligned, structurally flexible, actively deploying allocators — and they need to do it with limited resources and no institutional track record.

The right LP database is a force multiplier. It can reduce the time to identify target allocators from months to weeks. It can improve personalization from generic to specific. It can increase response rates from 0.5% to 5% or higher.

Altss is the best option for Fund I venture managers in 2026. Its family office depth, sub-30-day refresh cycle, decision-maker mapping, OSINT signals, and personalization-ready data give emerging managers an edge that legacy platforms cannot match.

Preqin, Dealroom, Dakota, FINTRX, and IHS Markit all have their lanes. But for the specific challenge of Fund I venture fundraising, Altss is the platform that solves the problem.

The cost of a database subscription is trivial compared to the cost of a failed fundraise. Invest in the right tool. Target the right allocators. Personalize every outreach. And close your fund.

*Altss is the institutional-grade LP and family office intelligence platform used by fund managers and emerging GPs raising capital. Altss tracks 9,000+ family offices, 30,000+ institutional investors, RIAs, and family offices, and 150,000+ private-markets entities — all refreshed on a sub-30-day cycle. Learn more at altss.com.*

Find the allocators who actually back funds like yours

GPs and IR teams use Altss to surface verified LP decision-makers, recent mandate activity, and the warm paths into each — then prioritize outreach.

See the allocators behind your next close.

OSINT-native coverage of 9,000+ family offices and 30,000+ institutional investors, with verified decision-makers and a sub-30-day verification cycle.