US Public Pension Commitments in Q1 2026

By Alex Dovzhenko · LP Intelligence · April 23, 2026 · 12 min read · Data as of April 23, 2026

Alex Dovzhenko writes Altss Insights, Altss's primary-source research on alternative-asset allocation. He covers LP behavior, consultant gatekeepers, and emerging-manager capital flows. Prior to Altss he built quantitative pension analytics for a global placement firm.

Across 12 US public pension systems whose Q1 2026 or early-Q2 primary-source disclosures were reachable in this window, 26 individual private-markets commitments land at $4.67 billion — from New York State Common Retirement Fund, Pennsylvania PSERS, Connecticut Retirement Plans & Trust Funds, Florida SBA's FRS Pension Plan, and the $316 billion New York City Bureau of Asset Management. Credit dollars ran at 88% of private-equity dollars across the systems publishing ticket-level commitments. Connecticut's 2026 pacing plan allocates more to credit ($2.75B) than to private equity ($2.70B) for the first time in the fund's history. On April 16, NYC Comptroller Mark Levine announced a $4 billion four-year commitment by the five NYC pension funds to finance affordable housing — the largest single Q1/early-Q2 2026 US pension-system housing commitment on the record. Ninety-five percent of primary-source emerging-manager capital flowed through three gatekeepers: GCM Grosvenor, the RockCreek Group, and Muller and Monroe. Mature programs are trimming PE targets. Mid-cycle programs keep expanding.

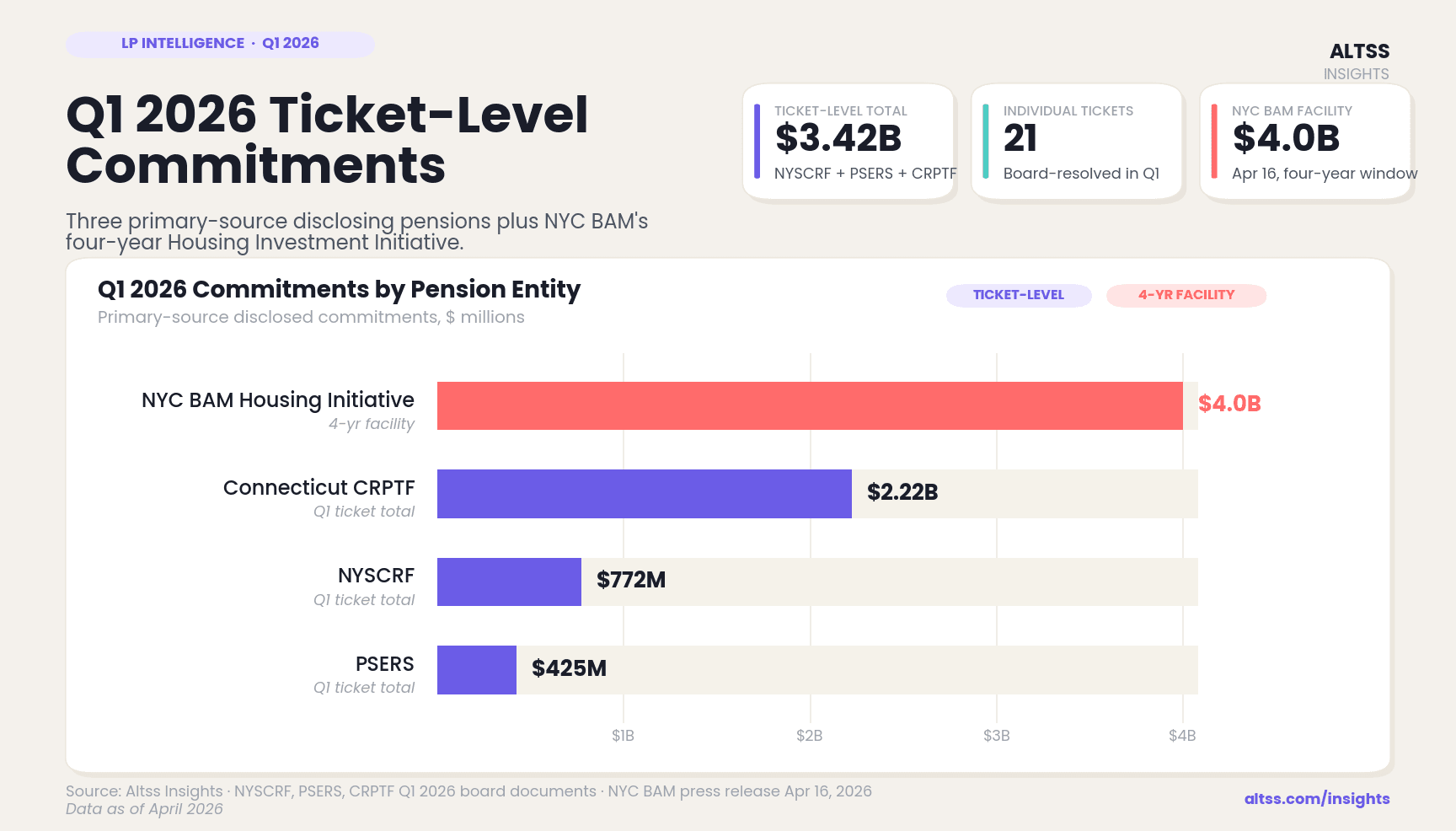

Twelve systems on the primary-source record. Three publish tickets the day they approve them.

This piece draws on primary-source documents from twelve US public pension systems: NYSCRF, PSERS, CRPTF, TX TRS, APFC, MSRPS, NYC BAM (NYCERS, TRS, Fire, Police, BERS), FL SBA, MN SBI, Ohio PERS, CalPERS, and OTRS. Three publish specific fund names and dollar amounts on or near the board-vote date: NYSCRF (monthly transaction reports), PSERS (individual board resolution PDFs), and CRPTF (Treasurer's press release at each IAC meeting). Together these three systems approved 21 private-markets commitments totaling $3,421.76 million in Q1 2026 and the first three weeks of April, each backed by a primary document.

NYSCRF contributed seven private-markets tickets totaling $771.76 million across its January and February 2026 Monthly Transaction Reports: $350M to Apollo Hybrid Value Fund III (via the Apollo Excelsior, L.P. fund-of-one), $200M to Kennedy Lewis Management's KLIM Delta Excelsior Fund, $150M to Leonard Green & Partners' Sage Equity Investors, and four tickets totaling $71.76M through the Muller and Monroe-intermediated M2 NY Pioneer Fund III EM sleeve — Oceans Ventures Fund III ($25M), Cross Rapids Capital Partners I ($15M), Palm Peak Capital Fund I ($15M), Demopolis Equity Partners Fund I ($16.76M).

PSERS approved three commitments totaling $425M at its March 19 Investment Committee: $150M to DRA Growth and Income Fund XII, $200M to LS Power Equity Partners VI, and $75M to Warwick Partners V. Aksia, LLC was the consultant of record on all three. One catch: the PSERS press release body names the second commitment "LS Power Equity Partners IV"; Resolution 2026-17 — both filename and RESOLVED clause — names "LS Power Equity Partners VI, L.P." Three trade-press summaries inherited the typo. The board-approved fund is VI.

Connecticut contributed eleven commitments totaling $2,225M across two IAC meetings. January 14: $425M to CRPTF-GCM Emerging Manager Partnership 2026-1 (PE) and $250M to its RE sister sleeve CRPTF-GCM Emerging Managers 2026-2, $350M across two I Squared Capital infrastructure funds, $550M across two Eagle Point Credit vehicles, and $300M to CRPTF-RockCreek Emerging Manager Partnership Series II for senior credit. March 11: $200M each to Bregal Sagemount V-B, HarbourVest's Dover Street XII, and HarbourVest's Secondary Overflow Fund VI, plus a $50M top-up on Artemis Real Estate Partners Healthcare Fund III.

NYC's $4 billion four-year housing commitment is the single largest Q1/early-Q2 ticket on the record.

On April 16, 2026, NYC Comptroller Mark Levine unveiled the NYC Housing Investment Initiative — a $4 billion commitment to be deployed across the five NYC pension funds (NYCERS, TRS, Fire, Police, BERS) over the next four years at roughly $1B per year. First-tranche announcements: $750M of direct BAM-sourced investments headed to the pension boards for approval (mixed-income housing, preservation, office-to-residential conversions), and a $500M expansion of the Public Private Apartment Rehabilitation program administered by the Community Preservation Corporation, with a 36-month rate lock and 40-year amortization. Additional capital flagged for the AFL-CIO Housing Investment Trust.

The scale is material. Current NYC five-system residential portfolio: $2.8B at end-2025. The Initiative more than doubles it. The April 16 $1.25B first tranche alone exceeds the combined Q1 2026 ticket flow at CRPTF or PSERS. It is the largest single Q1/early-Q2 2026 primary-source commitment by a US public pension system on the record for this piece.

The release also locks in a CIO transition. Monte Tarbox — interim BAM CIO since the start of 2026 — was named permanent CIO on March 31, 2026 after three decades in institutional pension roles (former president AFL-CIO Investment Trust Corporation, ED NEBF, CIO Machinists National, PBGC Advisory Committee). The Housing Initiative is his first major portfolio expansion as permanent CIO. It is the only commitment in the primary-source window that belongs to a CIO confirmed within the prior 60 days.

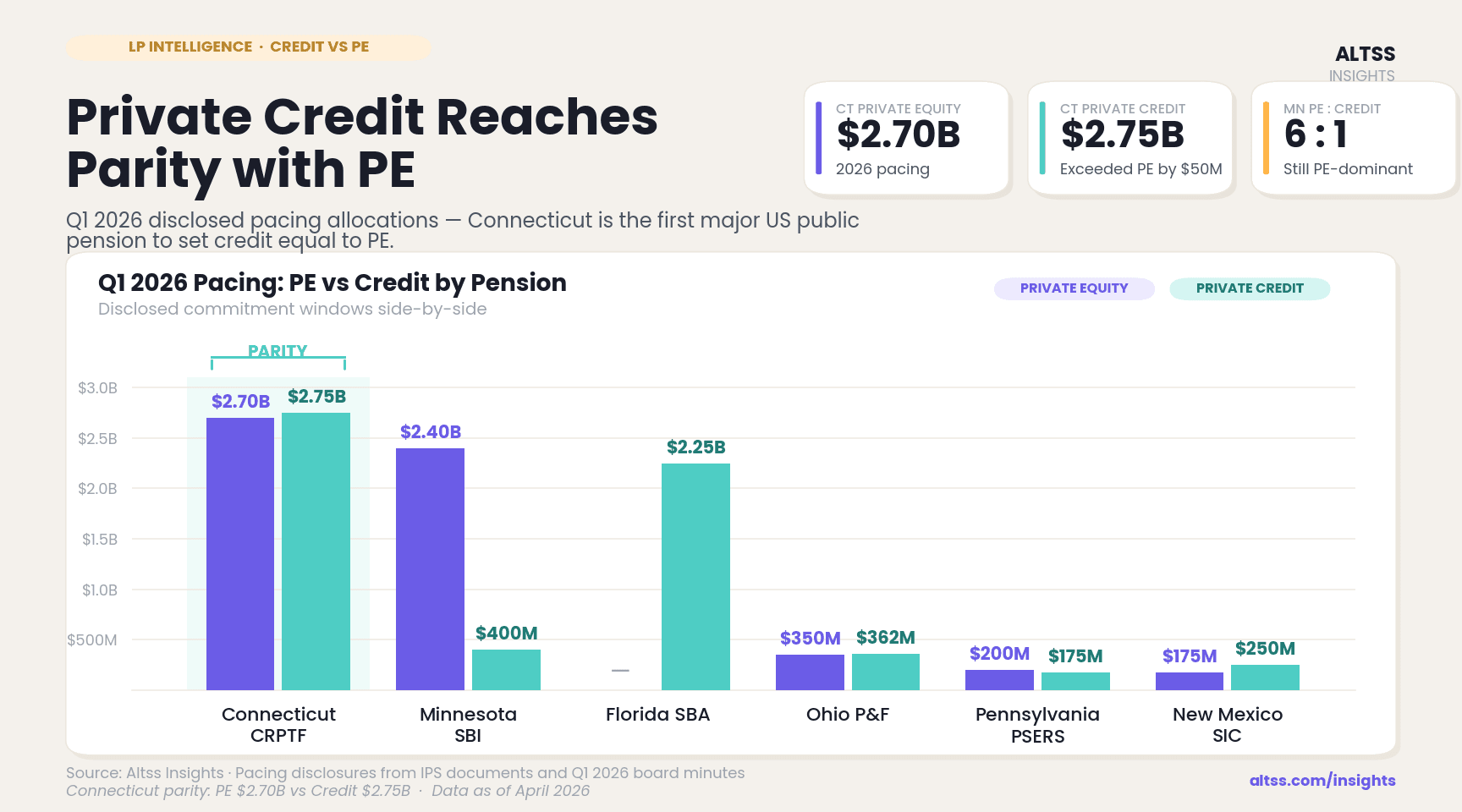

Credit runs at 88% of PE dollars across the three ticket-disclosing systems.

Aggregate the Q1 2026 commitments across NYSCRF, PSERS, and CRPTF and the private-credit column lands at $1,100 million against $1,246.76 million in private equity. Credit is running at 88% of PE dollars. Historically, credit has sat at 25–40% of PE dollars at US public pension systems. The shift is not noise.

At CRPTF the pattern is cleaner. Connecticut's 2026 pacing plan — published with the January 14 release — allocates $2.75 billion to credit versus $2.70 billion to private equity. Credit pacing exceeds PE pacing for the first time in the fund's modern history. Treasurer Erick Russell has said the long-term CRPTF credit target doubles to 10% (from 5%); the pension's Sept 30, 2025 allocation to the segment was near 3%. The compressed path to target — five years, doubling — forces a pacing plan that leads with credit.

At NYSCRF the Q1 distribution is starker: $550M in credit tickets ($350M Apollo Hybrid Value III + $200M KLIM Delta Excelsior) against $221.76M in private equity. PE tickets at NYSCRF in Q1 were smaller and flowed primarily through the M2/Muller and Monroe EM sleeve. At PSERS the question doesn't apply cleanly — the March 19 ticket set was skewed to real estate and infrastructure (energy), without a credit line item. At Florida SBA's March 30 Investment Advisory Council, the Active Credit SIO John Mogg reported public and private credit delivered strong 2025 returns with default rates falling and tight spreads across segments — consistent with the direction CRPTF is leaning into.

The ratio tells a consistent story across systems with different fiscal years, different governance structures, and different consultant relationships: when LPs have pacing flexibility, they are pacing credit harder than PE.

"Primary-source discipline converts a press-release typo to a verified fund name. The board approved LS Power VI, not IV. That's what reading the resolution instead of the summary gets you."

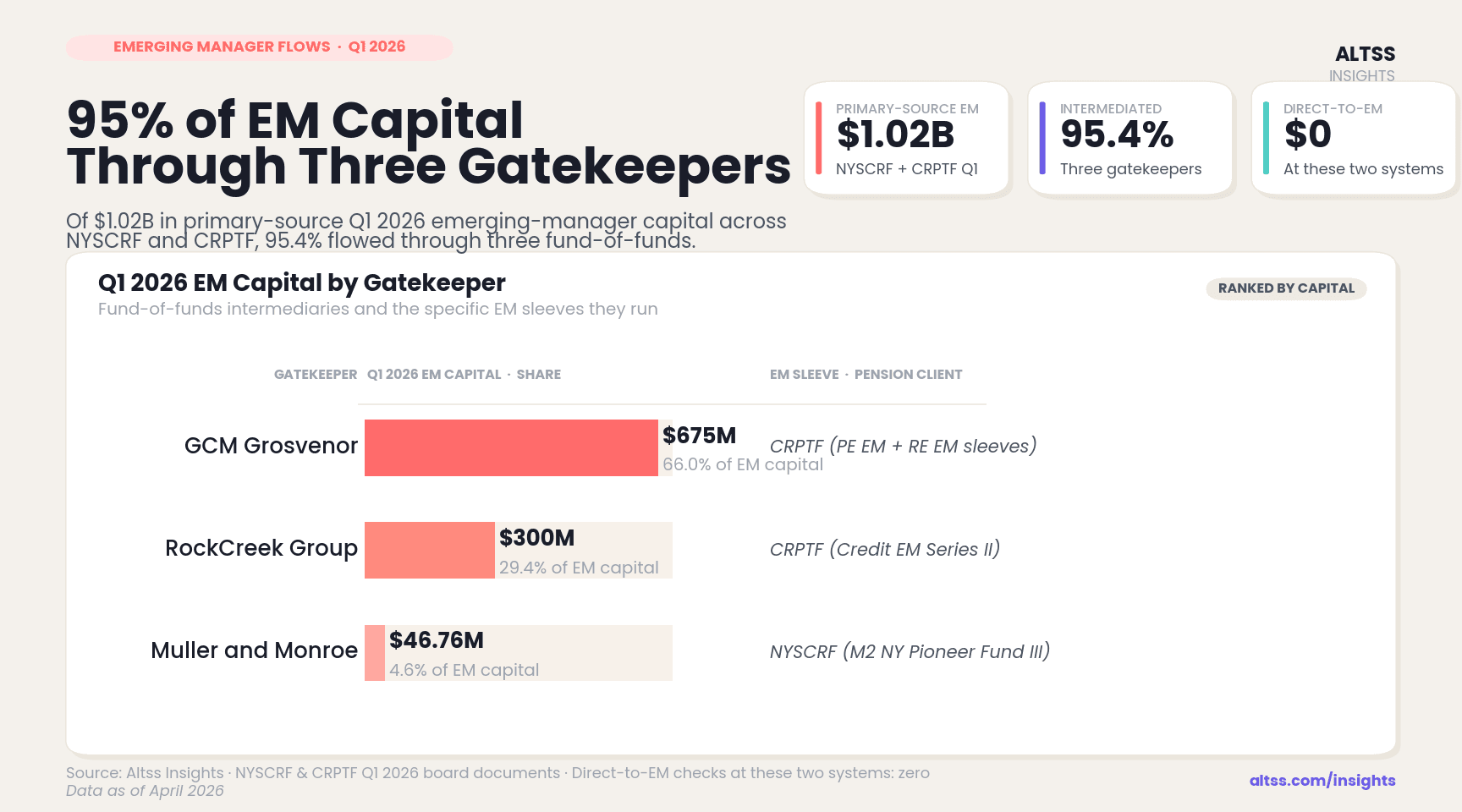

Ninety-five percent of primary-source EM capital flows through three gatekeepers.

Of $1,021.76 million in primary-source Q1 2026 emerging-manager capital across NYSCRF and CRPTF combined, $975M — 95.4% — was intermediated through three gatekeepers: GCM Grosvenor ($675M across CRPTF's PE and RE sleeves), the RockCreek Group ($300M via CRPTF's Credit EM Series II), and Muller and Monroe ($46.76M via NYSCRF's M2 NY Pioneer Fund III). The balance — $0 of direct-to-emerging-manager commitments — is instructive. In the systems that publish granular commitment data, every dollar of 2026 EM capital passed through an intermediary.

CRPTF is the clearest case. GCM Grosvenor alone received $675M at a single Investment Advisory Council meeting (January 14), split $425M to the PE-dedicated sleeve and $250M to the real-estate sleeve. The effect: a CRPTF emerging manager program operates as three pooled vehicles — one GCM-managed PE sleeve, one GCM-managed RE sleeve, one RockCreek-managed credit sleeve — and a first-time manager's path to the fund runs through three intermediary relationships, not the Treasurer's office directly.

At NYSCRF the structure is narrower in size but identical in shape. The three $15M-ish EM tickets in February — Cross Rapids, Palm Peak, Demopolis — all cleared through Muller and Monroe's M2 NY Pioneer Fund III. No direct-to-manager EM check appeared in the January or February reports.

The pipeline visibility around it matters. On January 28, NYC Comptroller Levine, NYS Comptroller DiNapoli, NYSTRS, and NYSIF announced the second annual Emerging Managers Week held the week of February 9, 2026, with a combined LP universe "representing more than $1 trillion in assets." Four conferences over four days: NYSIF's 16th MWBE Symposium, NYC BAM's 2026 Annual Diverse & Emerging Managers Conference, NYSTRS's 16th Annual MWBE Conference in Troy, and NYSCRF's 19th Annual Emerging Manager and MWBE Conference. The pipeline is coordinated; the capital is gatekeeper-intermediated.

The implication for a first-time or second-fund GP: the LP on the check isn't the pension. It's the gatekeeper. At the three systems in this primary-source commitment dataset, the underwriting and manager selection decision lives at GCM, RockCreek, or Muller and Monroe. Emerging-manager fundraising without an established relationship with one of these three is structurally harder at NYSCRF and CRPTF in 2026 than it was in 2023, when more direct allocations appeared in NYSCRF reports.

Mature programs trim. Mid-cycle programs expand.

Connecticut's pacing plan calls for PE to reach 15% of total fund assets by the end of 2028, up from 11% at September 30, 2025 — a four-percentage-point expansion over three years.

At APFC the direction of travel is the opposite. On February 25, APFC released the summary of its February 23–24 quarterly meeting. CIO Marcus Frampton and CRCO Sebastian Vadakumcherry presented two asset-allocation options alongside the current target. Per the release, both alternatives "increase investments in public markets and fixed income, offset by reducing exposure to private markets." The board votes May 26–27 in Valdez. The Fund is in its 50th year.

At Ohio PERS the PE page (unaudited Q2 2025) confirms PE at $16.2B or 14.3% of the DB Fund — sitting just above the 14% target the board voted to in November 2025 (down from 15%). Q2 2025 PE returns ran 2.03% against a 4.16% benchmark; YTD 6.57% against 6.98%. Both periods underperformed. Oregon PERF's consultant Meketa flagged PE overweight as the largest Q3 2025 performance detractor at the Oregon Investment Council, a position the OIC has continued to weigh.

The bigger systems hold. CalPERS CIO Stephen Gilmore presided over the Investment Committee's March 16–17 meeting, which concluded a first-reading review of the Total Fund Policy — allocation discussion is at first-reading stage, not vote-ready. FL SBA PE SIO John Bradley reported Q3 2025 PE performance up 2.6% with 2025 net distributions of $1.0B; the five-year RE pacing model proposes $960M-$1,220M of FY26 core RE capital plus $710M-$900M non-core. No PE target cut. NYSCRF holds PE at 15%. Maryland SRPS's open sessions confirm Vice Chair Brooke Lierman, Acting ED Jonathan Martin, Deputy CIO Robert Burb, and fiscal-year-to-date December performance of +6.46% without a target change.

The pattern holds across program maturity, not market conditions. Programs under fifteen years are building PE exposure toward targets. Programs over twenty-five years are holding, trimming, or debating a trim. CRPTF is scaling into the same vintage years APFC is scaling out of.

Aksia is the only consultant named on every ticket at a single primary-source system.

At PSERS, Aksia, LLC was the recommending consultant on all three March 19 commitments — DRA XII, LS Power VI, and Warwick V. Three out of three. No other external consultant appeared as recommender on the Q1 2026 PSERS private-markets ticket set.

At CRPTF the consultant seat is structured differently: recommendations to the IAC flow through the Treasurer's internal Pension Funds Management Division, and the EM sleeves outsource manager selection to the GCM and RockCreek gatekeepers directly rather than to an external consultant. Aksia, Meketa, Cambridge, and NEPC do not appear as named recommenders in the January 14 or March 11 IAC releases. At NYSCRF the Monthly Transaction Reports do not cite an external consultant per ticket. At Florida SBA the real-estate pacing model is prepared by Townsend.

One Q1 2026 consultant-coverage story sits outside the commitment flow. Oklahoma Teachers Retirement System's April 22, 2026 board agenda includes an Investment Committee item captioned "Discussion and possible action on final selection of Investment Consultant(s)" together with a separate item on "Investment Consultant FY2026 annual review process." OTRS is actively running a consultant RFP. The market is concentrated already; a new selection at OTRS would further narrow the top-of-funnel for external consultants.

For a GP fundraising a 2026 vintage the pragmatic read: Aksia has the highest visible PSERS concentration across Q1 primary-source tickets; GCM Grosvenor and RockCreek control the Connecticut EM funnel; Muller and Monroe controls the New York EM feeder. Four names account for every external-party seat on the commitments verified against board documents in this window.

The trade-press universe is broader. The board-document universe is the one that prices.

The trade-press record reports Q1 activity at Texas TRS, LACERA, Texas MRS, Ohio Police & Fire, and others — typically citing totals in the $800M to $4.3B range per system. Those numbers are in the dataset filed with this piece, flagged `trade_press_only` or `unreachable_in_session`. They are not cited in this article because they did not survive the primary-source test. The Texas TRS February 12–13 board book (281 pages) does not contain "Cerberus" or "Carlyle" despite Dakota's January coverage citing a $1.1B round including both. The Oklahoma Teachers April 22 agenda confirms the prior board meeting was February 25, not January 28 as Dakota's reporting implied. Maryland SRPS's open sessions reference Investment Committee reports at a governance level but do not enumerate named fund commitments. The alleged "Cerberus Proper Partners" TX TRS commitment has no primary-source footprint; the resolution will only come when TRS publishes its Q1 2026 IMD quarterly report.

What this means for allocators.

If your pacing tilts 50/50 PE/credit, you are in line with where primary-source systems are setting 2026 pacing. If your PE-to-credit ratio is still 3:1, you are lagging where CRPTF is pointing. Credit pacing has caught PE pacing; it has not surpassed it in a way that implies rotation. If your EM fund-of-funds is not named GCM Grosvenor, the RockCreek Group, or Muller and Monroe, ask your peer systems why. If you run a PE program older than twenty-five years and have not reviewed your target in twelve months, your neighbors have — APFC, Ohio PERS, and Oregon PERF all sit within three percentage points of the same maturity curve point.

What this means for emerging GPs.

The LP on the check is almost certainly the gatekeeper. Zero direct-to-EM checks cleared at the three primary-source systems in Q1 2026. If your deck is not on the manager-review desk at GCM Grosvenor, the RockCreek Group, or Muller and Monroe, it is not being reviewed at NYSCRF or CRPTF.

Ticket sizes through intermediated sleeves run small. The three NYSCRF EM checks were $15M, $15M, and $16.76M. CRPTF EM sleeves are structured commitments — $425M PE, $300M credit, $250M RE — with GCM or RockCreek selecting the underlying managers. A first-time GP's shot at a $20–30M check through CRPTF runs through a gatekeeper process, not a Treasurer's Office conversation.

Credit EM mandates are now matched in size to PE EM mandates. CRPTF's RockCreek Credit EM Series II was $300M in 2026 — a step up from the historical tilt toward PE-only EM programs. The door is wider for emerging credit managers than it was in 2024. Mature systems trimming PE targets are where the next fundraise is harder; mid-cycle systems like CRPTF and expansions like NYC BAM's $4B housing initiative are the better doors.

Where to cross-check.

Altss maintains the primary-source consultant and LP dataset underlying this piece. Every dollar figure above traces to a URL in the Sources section. Every named fund has been verified against either a board resolution, an IAC release, a Monthly Transaction Report, or an Investment Advisory Council deck. Where a figure could not be verified to a board document — for Texas TRS, Texas MRS, LACERA, and others — the figure is not cited here, and is labelled `trade_press_only` or `unreachable_in_session` in the dataset filed alongside the article.

The quarter in one line.

Credit caught PE in the primary-source pacing, three gatekeepers caught 95% of emerging-manager dollars, mature programs caught the bottom of their PE appetite, and New York caught the year's biggest housing allocation.

Data as of April 23, 2026. Source: primary-source board documents at NYSCRF, PSERS, CRPTF, APFC, TX TRS, MSRPS, NYC BAM, FL SBA, MN SBI, Ohio PERS, CalPERS, OTRS.