How a single $65B AI round masked a steady, widening month of family-office direct activity, with IT back on top, ICONIQ running the AI thread, and sports infrastructure emerging as the breakout family-capital theme.

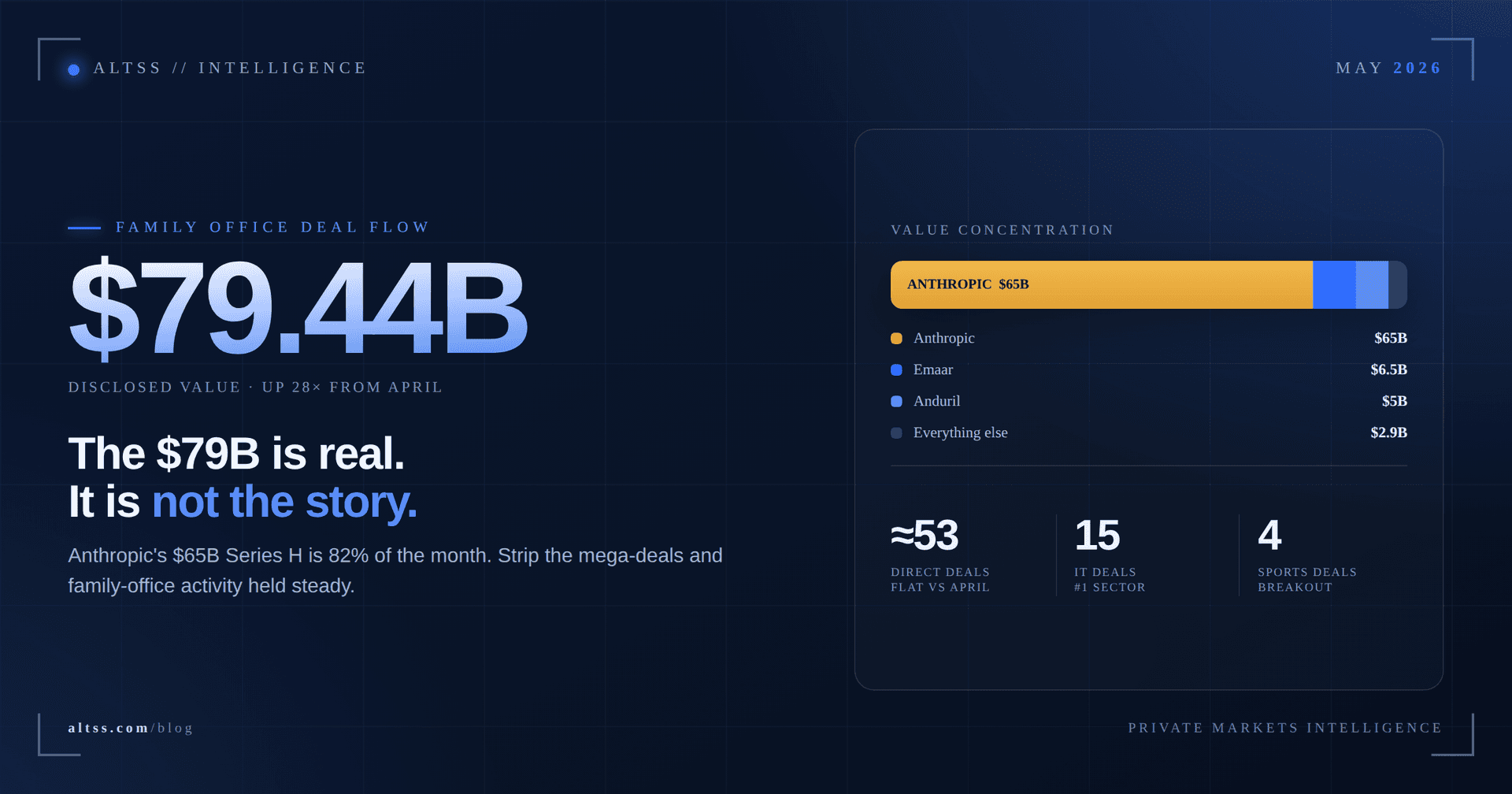

TL;DR: May 2026 looked, on the headline, like the biggest month since March, with disclosed value tied to family-office participation jumping to $79.44B from $2.86B in April. Strip out one round and that story collapses. Anthropic's $65B Series H accounts for roughly 82% of the month's tracked dollars on its own, and the top three transactions (Anthropic, Dubai Holding's $6.5B Emaar stake, and Anduril's $5B) explain about 96% of the total. Underneath the concentration, family-office direct activity held its cadence at about 53 deals, in line with April and well above March's 39. Three dynamics defined the month. First, Information Technology retook the sector lead with 15 deals, and ICONIQ Capital was the visible family-capital thread across the largest AI and payments rounds. Second, family and principal capital moved decisively into sports infrastructure, buying league rails, athlete data, women's sports and emerging formats rather than just trophies. Third, principal vehicles ran control plays in media (Byron Allen into BuzzFeed, James Murdoch into New York Magazine and Vox) while founder-family offices kept seeding the frontier (Breyer in mRNA, the Nintendo and Supercell family offices in AI, Thiel in ocean-powered compute). All of this unfolded under a new Federal Reserve chair, sticky inflation, and the largest IPO in history loading into early June. The message for fundraising teams is unchanged: when headline venture dollars concentrate into a handful of frontier names, family-office direct activity is where breadth and early conviction actually live, and most of it never surfaces in a legacy database in time to matter.

Key data

Family-office direct investments in May 2026: about 53, broadly flat against the 55 Altss tracked in April and well above March's 39.

Disclosed value: $79.44B, a sharp jump from $2.86B in April, driven predominantly by one round.

Single largest driver: Anthropic's $65B Series H at a $965B post-money valuation, roughly 82% of May's disclosed total. ICONIQ Capital was among the lead investors.

Sector lead: Information Technology, 15 deals, reversing April's brief healthcare crossover.

Breakout theme: sports and entertainment, led by the Las Vegas Raiders stake sale, Pickleball Inc., PlayerData and Just Women's Sports.

The 8 most important family-office-backed moves of May 2026

1) ICONIQ co-leads Anthropic's $65B Series H, the largest AI round in history

On May 28, Anthropic closed a $65 billion Series H at a $965 billion post-money valuation, passing OpenAI to become the most valuable AI company in the world. The round was led by Altimeter Capital, Dragoneer, Greenoaks and Sequoia, with a second co-lead tier that included Capital Group, Coatue, D1 Capital Partners, GIC, ICONIQ and XN. The round also folds in $15 billion of previously committed hyperscaler capital, including $5 billion from Amazon, so the fresh capital is meaningfully below the $65 billion headline. Anthropic CFO Krishna Rao framed the raise around adoption, saying Claude is "increasingly indispensable to our growing global community of customers."

Why it matters for LP intelligence

ICONIQ's presence in the co-lead tier is the family-capital signal, not the $65 billion. ICONIQ is the most active multi-family-office platform in the market, and it had already led Anthropic's Series F in 2025. Its return as a co-lead at the $965 billion mark confirms that the largest family-office aggregator is comfortable underwriting frontier AI at a near-trillion valuation, one round before a likely IPO. For GPs raising AI or growth-equity vehicles, ICONIQ is the reference node: it is simultaneously deploying across PE, credit, real assets, secondaries and GP stakes, which means the right entry point is the specific vehicle, not "ICONIQ" as a single LP. Mapping which ICONIQ fund touches your strategy is the difference between a meeting and a dead end.

2) Michael Dell and a Silver Lake group take 25% of the Las Vegas Raiders at a $9.9B valuation

A consortium led by Silver Lake co-CEO Egon Durban agreed to acquire a 25% stake in the Las Vegas Raiders, valuing the franchise at $9.9 billion, with Michael Dell among the individual investors taking a position alongside Blackstone's Joseph Baratta. The equity came from minority holders, not from controlling owner Mark Davis, who remains in control. Six investors now hold a combined 25.3%, and Durban retains a right of first refusal to acquire control should Davis ever sell.

Why it matters for LP intelligence

This is principal-family capital (Dell via his investment vehicle) buying into the single most defensible asset class in sports: an NFL franchise. The pattern matters more than the trophy. Family principals are increasingly treating top-tier sports equity as an inflation-resistant, scarcity-driven store of value, and the NFL's loosened rules on institutional and limited-partner ownership are opening the door. For managers raising sports, media or real-asset vehicles, the Raiders deal is the high end of a barbell whose other end (data, leagues, women's sports) showed up across the rest of the month.

3) Dundon and Apollo put $225M into Pickleball Inc., consolidating a sport into one platform

Pickleball Inc., the newly formed parent of the PPA Tour and Major League Pickleball, raised a $225 million structured investment led by Apollo Sports Capital with Dundon Capital Partners, valuing the company at $750 million. Tom Dundon and the Pardoe family remain majority owners and rolled additional pickleball assets (facilities, retail, technology) into the platform. CEO Connor Pardoe called it "a seismic day for the rapidly growing business of pickleball."

Why it matters for LP intelligence

This is the clearest operating-business sports bet of the month. Dundon, an owner of the Carolina Hurricanes and Portland Trail Blazers, is not buying a team, he is consolidating an entire sport's commercial stack (tours, leagues, facilities, retail, technology) into one platform. For GPs, the signal is that principal sports capital is moving from franchise ownership to category ownership, and the families writing these checks want operating control and roll-up optionality, not passive minority positions. That changes how you structure co-invest if you want them alongside your fund.

4) Byron Allen's family office takes control of BuzzFeed for $120M

Allen Family Digital, an affiliate of Byron Allen's family office, closed its acquisition of about 51% of BuzzFeed for $120 million, structured as $20 million in cash and a $100 million promissory note, with Allen becoming chairman and CEO. The transaction was disclosed and closed through public SEC filings in May, landing as BuzzFeed faced a missed debt payment and a near-term liquidity squeeze. Allen, who praised outgoing founder Jonah Peretti as "a great visionary," is steering the company toward free streaming and AI-powered media.

Why it matters for LP intelligence

This is a family office using a structured, low-cash-outlay control deal to take over a public company at a distressed valuation. The structure (mostly a five-year note) is the lesson: principal capital can acquire control without writing a full cash cheque, which is exactly the kind of creative balance-sheet move institutional buyers are often too constrained to make. For managers in media, special situations or distressed equity, the takeaway is that family offices are now credible lead acquirers in turnaround situations, not just minority co-investors.

5) James Murdoch's Lupa Systems acquires New York Magazine, Vox and the Vox podcast network

Lupa Systems, James Murdoch's media and technology holding company, agreed to acquire New York Magazine, the Vox Media Podcast Network and Vox from Vox Media in a deal reported at more than $300 million. The properties will operate as a Lupa subsidiary, returning New York Magazine to the Murdoch family for the first time since 1991. Murdoch said the deal "aligns well with our existing holdings and investments."

Why it matters for LP intelligence

Murdoch's Lupa is a textbook post-liquidity single-family vehicle (built after he exited the family media empire for roughly $3.3 billion) now deploying into the sectors he knows best. The deal sits alongside Allen's BuzzFeed move as a second principal-family media control transaction in a single month, both betting on premium editorial and audio at a moment when public-market media valuations are depressed. For GPs, the structural read is that founder-family media capital is counter-cyclical: it buys editorial assets when institutional sentiment is worst.

6) The Nintendo founding family office backs Decart's $300M Series B

Decart, a continuously refreshed AI world-model lab, raised a $300 million Series B led by Radical Ventures at about a $4 billion valuation. The Yamauchi No.10 Family Office, the Tokyo vehicle of Nintendo's founding family, participated alongside NVIDIA, Sequoia, Benchmark and angels including Andrej Karpathy and Michael Eisner, with Amazon joining as a strategic chip partner.

Why it matters for LP intelligence

This is a founding-family office reaching into the absolute frontier of AI (world models for video, gaming and robotics) where its operating heritage gives it genuine edge. The Yamauchi office is small, Tokyo-based, and invisible to most Western LP datasets, yet it sits on a cap table next to NVIDIA. For GPs raising AI, gaming or robotics strategies, the lesson is that the most valuable family-office LPs for a given thesis are often the operating families whose original business maps onto it, and those are precisely the offices legacy databases miss.

7) Peter Thiel leads Panthalassa's $140M to build ocean-powered AI compute

Panthalassa, an Oregon-based ocean-technology company, raised a $140 million Series B led by Peter Thiel, with John Doerr, Marc Benioff's TIME Ventures, Max Levchin's SciFi Ventures and Founders Fund participating, to build autonomous wave-powered nodes that perform AI inference at sea and transmit results via satellite.

Why it matters for LP intelligence

The most interesting AI bet of the month was not a model, it was the energy under one. Principal capital (Thiel, Doerr, Benioff, Levchin) is now underwriting the power and cooling layer of AI rather than the application layer, because compute is constrained by energy, not ideas. For GPs raising AI-infrastructure, energy-transition or deep-tech vehicles, Panthalassa confirms that the billionaire-principal tier wants AI exposure with a hard-asset, infrastructure-grade moat. That is the pitch that lands with these offices, not application software with uncertain unit economics.

8) Breyer Capital leads ParcelBio's $13M seed in programmable mRNA

ParcelBio launched with a $13 million seed led by Breyer Capital, Jim Breyer's family investment vehicle, with General Catalyst and Y Combinator participating, to advance programmable mRNA and in vivo CAR-T programs for autoimmune disease and oncology. CEO David Weinberg framed the opportunity bluntly, noting that "mRNA has transformed medicine, but today's technologies are fundamentally limited."

Why it matters for LP intelligence

Breyer leading at seed is the family-office-as-price-setter pattern: a sophisticated principal vehicle taking the lead order in a deep-science round at the earliest stage, where the family acts as anchor rather than passenger. For managers raising biotech or life-sciences vehicles, ParcelBio is a reminder that the best family-office entry point is often a thesis-driven seed lead, and that offices like Breyer's are competing with sector VCs for those positions, not just co-investing behind them.

The $79 billion is real, but it is not the story

On paper, May was the biggest month since March, with disclosed value moving from $2.86 billion in April to $79.44 billion. In practice the month was one cheque. Anthropic's $65 billion Series H accounts for about 82% of the monthly total by itself. Add Dubai Holding's $6.5 billion Emaar stake and Anduril's $5 billion Series H, and three transactions explain roughly 96% of the figure.

That does not make the number wrong. It makes it top-heavy, and it is exactly the distortion the April review flagged when it noted that March's totals were inflated by OpenAI's $122 billion round. When frontier AI absorbs tens of billions in single rounds, monthly dollar totals stop describing where families are actually deploying. This is why Altss leads with deal count, not dollars. On that measure, May was steady: about 53 direct investments, in line with April, across a widening set of themes.

IT retook the lead, and ICONIQ was the through-line

Information Technology reclaimed the top sector slot in May with 15 family-office-linked deals, reversing April's brief healthcare crossover. The driver was frontier AI, defense technology, enterprise software and payments.

ICONIQ was the visible family-capital thread, named among the co-leads of Anthropic's $65 billion Series H and continuing as an existing backer in Primer's $100 million Series C, which was led by Sofina. The detail matters for an honest read, because the other two landmark technology rounds of the month ran through different leads. Anduril raised $5 billion at a $61 billion valuation led by Thrive Capital and Andreessen Horowitz, one of the largest defense-technology raises on record; CEO Brian Schimpf noted that in 2017 "defense was not a category that attracted significant venture investment." Sierra, Bret Taylor's enterprise AI agent company, raised a $950 million Series E at a $15.8 billion valuation led by Tiger Global and GV. Both deals are central to the AI and defense narrative, but neither names a family office as a disclosed lead, so we treat them as market context rather than as family-office direct deals. We flag this deliberately: some trackers attribute family-office participation to these rounds, but it does not appear in primary disclosure, and we would rather under-claim than overstate the cap table.

The frontier-adjacent family money showed up earlier in the stack. Decart's $300 million Series B brought in the Nintendo founding family office. Panthalassa's $140 million put Thiel, Doerr and Benioff into ocean-powered compute. And London's CodeWords closed a $9 million seed led by Visionaries, with Illusian, the family office co-founded by Supercell CEO Ilkka Paananen, participating. The common profile is unmistakable: operating families whose original businesses (gaming, software, payments) map directly onto the AI thesis they are now funding.

Sports became the breakout family-office theme

Family principals have always owned trophies. May was different because the money moved past the trophy and into the operating infrastructure around sport.

At the top end, the Silver Lake group's 25% Raiders stake put Michael Dell's principal capital into an NFL franchise at a $9.9 billion valuation. One tier down, Apollo Sports Capital and Dundon Capital Partners put $225 million into Pickleball Inc. at a $750 million valuation, consolidating the PPA Tour and Major League Pickleball into a single platform with Dundon and the Pardoe family retaining majority control.

The more telling deals were the smaller ones. PlayerData raised a $12 million Series A led by Pentland Ventures, Darco Ventures and Bolt Ventures, with Kevin Durant's 35V joining as a strategic investor. Bolt Ventures is David Blitzer's private investment platform, and it surfaced again days later in sports media, where Just Women's Sports added a new raise in late May with Bolt among the backers. Two athlete-and-principal capital vehicles (Blitzer's Bolt, Durant's 35V) appeared across athlete data and women's sports in the same window.

Why it matters for LP intelligence

The throughline is that family money is no longer just buying a seat in the owner's box. It is buying the league rails, the media rights, the women's-sports growth curve, the athlete-performance data and the emerging-format upside, as operating businesses. For GPs raising sports, media or consumer vehicles, the relevant LP map now includes athlete-founded vehicles (35V), sports-principal family offices (Blitzer, Dundon) and tech-principal families (Dell) that move across the entire stack from franchise equity to seed-stage sports tech. These vehicles increasingly lead and structure deals, which means they can compete with your fund for the best positions and co-invest alongside it on the rest.

Climate, the blue economy, and the Walton thesis

In climate and ocean infrastructure, Lukas Walton's Builders Vision was active twice. It backed CREW Carbon's $25 million Series A package (a $19 million equity round led by Burnt Island Ventures plus $6 million in non-dilutive funding) and joined ECOncrete's marine-infrastructure fundraise alongside Barclays Climate Ventures and the Prince Albert II of Monaco Foundation's ReOcean Fund.

Why it matters for LP intelligence

Builders Vision is the canonical impact-anchored single-family office, managing more than $15 billion of Walton capital across energy, oceans, and food and agriculture. CIO Noelle Laing, promoted in early 2025, consolidated the platform's investment strategies into a single practice overseeing nearly 30 investors, after running Builders Initiative's $1.7 billion endowment. Two ocean and decarbonization checks in a single month confirm a durable, thesis-driven mandate that does not chase the AI cycle. For GPs raising climate, blue-economy or hard-tech vehicles, Builders Vision is the model of a family office that will lead and anchor in sectors most institutional capital still treats as concessionary, and the co-investors it travels with (Burnt Island, the Monaco foundation's ReOcean Fund) form a discoverable warm-path cluster around ocean and water technology.

Media control, and insurtech as the family-office-as-participant pattern

The two media control deals (Allen into BuzzFeed, Murdoch into New York Magazine and Vox) are covered above as principal-family takeovers of distressed editorial assets. The pattern to file is structural: founder-family media capital is counter-cyclical and increasingly comfortable taking control, not minority stakes.

Insurtech showed the opposite, quieter pattern. Corgi raised a $160 million Series B at a $1.3 billion valuation led by TCV, with Alpha Square Group, Paolo Agazzone's family office, participating. Here the family office is a participant in an institutionally led round rather than the lead, which is the more common shape of family-office venture activity and a useful reminder that most family-office "participation" is exactly that: a position in a round someone else priced. For LP-mapping purposes, distinguishing lead-capable family offices (Breyer, ICONIQ, Builders Vision, Premji) from participant offices (Alpha Square in Corgi, ICONIQ in Primer) is the single most useful cut, because it tells you who you are actually pitching and how much they can write.

The Emaar reshuffle, and why we flag sovereign-family capital separately

Dubai Holding acquired a 22.27% stake in Emaar Properties from the Investment Corporation of Dubai for about $6.5 billion, lifting its total holding to 29.73% and making it Emaar's largest shareholder. We count it, because Dubai Holding is the ruling family's holding vehicle and the transaction is squarely sovereign-adjacent family capital, but we call it out separately for two reasons. First, it is an intra-government transfer between two Dubai state-linked entities, not a competitive market round, so it tells you little about where family offices are forming new conviction. Second, at $6.5 billion it is the second-largest line in the month and would badly distort any month-over-month value comparison if folded into the venture and growth totals. This is the same discipline we apply to Anthropic, the Raiders and BuzzFeed: counted, but quarantined from the underlying cadence.

Direct investing is now the default, not the exception

The structural backdrop to every deal above is that family offices have spent a decade building the internal capability to lead direct transactions, and May confirmed the trend is accelerating rather than plateauing. The most sophisticated offices now run private-equity-like teams that source, price and structure their own deals, taking the lead order rather than following a fund in. That is the difference between a Breyer leading a seed and a generalist office writing a pro-rata check behind one.

That is the through-line connecting ICONIQ co-leading the largest AI round, Breyer leading a deep-science seed, Allen and Murdoch running control plays in media, and Dundon consolidating an entire sport: these are not passive co-investors writing pro-rata checks behind a fund, they are price-setters. For GPs, the implication is uncomfortable but clear. The value proposition of a blind-pool fund now has to clear a higher bar, because the most sophisticated family offices will increasingly ask why they should commit to your fund when they can access the deal directly. The managers who win family-office capital in this environment are the ones who offer something direct investing cannot: differentiated sourcing, sector access, or earlier-stage deal flow that the offices cannot reach alone.

The macro backdrop: a new Fed chair, sticky inflation, and the largest IPO in history

May unfolded against a meaningfully different monetary picture than the start of the year. Kevin Warsh took over as Federal Reserve chair on May 22, inheriting a divided committee with the federal funds target held at 3.50% to 3.75% after the April hold, inflation running around 4.2% year over year, and energy prices elevated on the back of regional conflict. Markets moved to near-certain pricing of no change at the June meeting, with the committee signaling a formal shift away from any easing bias. For family offices, higher-for-longer rates keep private credit and structured, note-funded acquisitions (exactly the structure Byron Allen used for BuzzFeed) attractive, while pressuring long-duration real estate and pushing patient capital toward scarcity assets and infrastructure with hard-asset moats.

The larger event loading into early June was liquidity. SpaceX publicly filed its S-1 on May 20 and lined up a Nasdaq listing under the ticker SPCX, pricing in mid-June at roughly $1.75 trillion and targeting a $75 billion raise, the largest IPO in market history. Because SpaceX absorbed xAI in an earlier all-stock merger, family offices that backed xAI's prior rounds now hold SpaceX equity that becomes liquid at listing. Layer in Anthropic's own IPO runway (widely expected to follow its $965 billion Series H), and the back half of 2026 is set up to generate a wave of realized gains that flows straight back into family-office commitment capacity.

Why it matters for LP intelligence

The 90 days after a major tech IPO are historically the highest-conversion window for LP commitments from family offices that sat on the pre-IPO cap table. Offices holding SpaceX or xAI positions are about to mark large unrealized gains to realized, and the first allocations of that capital will go to managers who built the relationship before the liquidity event, not after. Tracking which family offices hold SpaceX, xAI and Anthropic exposure, and building the outreach calendar around the settlement dates, is one of the highest-leverage prospecting moves available in the second half of the year.

Notable absences and transitions

Gulf sovereign and Asian SFO leadership was quieter in the disclosed set. After a first quarter in which Gulf sovereign-adjacent vehicles and large Asian single-family offices (Mubadala, QIA, Temasek, Premji Invest) repeatedly led or anchored physical-AI mega-rounds, May's confirmed family-capital leadership concentrated in ICONIQ and US and European principal vehicles. We read this as cadence, not a change of thesis: these offices deployed heavily into AI infrastructure earlier in the year and are likely in portfolio-support mode, and absence from the disclosed May set is not the same as absence from the market.

Builders Vision under a consolidated CIO. Noelle Laing's consolidation of Builders Vision's investment strategies under a single practice (nearly 30 investors) is the kind of internal-structure signal that changes how managers should approach the office: decision-making is centralizing, which raises the bar for entry but also clarifies who to reach.

ICONIQ as the dominant aggregator of the month. With a 2025 vintage spanning PE, credit, real assets, secondaries and GP stakes and a co-lead in the largest AI round in history, ICONIQ was the single most active family-capital platform in May. For any manager targeting it, the work is identifying the right internal vehicle, not securing a generic introduction.

Additional verified deals worth tracking

Beyond the eight headline moves, several smaller rounds round out the family-capital census for the month and are worth tracking for the offices they expose:

Primer ($100M Series C, led by Sofina): ICONIQ continued as an existing backer in the AI-for-payments infrastructure company, a useful confirmation that ICONIQ's family-capital activity in May extended beyond the Anthropic headline into fintech infrastructure. Valuation was not disclosed.

CodeWords ($9M seed, led by Visionaries): Illusian, the Helsinki family office co-founded by Supercell CEO Ilkka Paananen, participated alongside a roster of operator-angels, a clean example of a gaming-founder office reaching into AI workflow automation.

PlayerData ($12M Series A) and Just Women's Sports (undisclosed): Both surfaced David Blitzer's Bolt Ventures, with Kevin Durant's 35V alongside in PlayerData, mapping the athlete-and-sports-principal capital cluster across athlete data and women's sports media in a single window.

CREW Carbon ($25M) and ECOncrete (undisclosed): Both surfaced Builders Vision, with the Prince Albert II of Monaco Foundation's ReOcean Fund alongside in ECOncrete, mapping the blue-economy and ocean-infrastructure cluster.

Corgi ($160M Series B, led by TCV): Alpha Square Group, Paolo Agazzone's family office, participated, an example of family-office venture activity in its most common shape, as a participant rather than a lead.

Individually, several of these are too small to move a global allocator's needle. Collectively, they show how family offices have become a default order in early-stage and growth financings that legacy LP datasets never capture at the deal level. If you are not tracking family-office vehicles round by round, you miss where future Series B and C ownership started.

What May tells us about family-office capital going into Q3 2026

1. AI conviction is real, but it is concentrating into compute and energy, not just models

ICONIQ co-led the largest AI round in history, and the most interesting frontier checks of the month went into the layer beneath the models: Decart's world-model infrastructure, Panthalassa's wave-powered compute, and the energy thesis those imply. For GPs raising AI-adjacent vehicles, the family-office question has shifted from "do you have AI exposure" to "do you have the infrastructure and energy exposure that the model layer depends on."

2. Sports infrastructure has crossed from trophy to operating business

The Raiders, Pickleball Inc., PlayerData and Just Women's Sports together mark a clear move from franchise ownership to category and infrastructure ownership. Principal and athlete-founded vehicles (Dell, Dundon, Blitzer's Bolt, Durant's 35V) are now leading and structuring these deals. Any manager raising a sports, media or consumer vehicle should treat these offices as both competitors for the best positions and co-investors for the rest.

3. Founder-family media capital is counter-cyclical and now takes control

Two principal-family media control deals in one month, both at depressed valuations, both structured for low cash outlay, confirm that founder-family media offices buy editorial and audio assets precisely when institutional sentiment is worst. For special-situations and media managers, these offices are credible lead acquirers, not passive co-investors.

4. The most valuable family-office LPs for a thesis are the operating families behind it

The Nintendo founding family in AI world models, the Supercell founder's office in AI workflow automation, Breyer in mRNA, Builders Vision in the blue economy. The pattern repeats every month: operating families deploy into the sectors their original businesses understand, and those offices are the ones legacy databases miss entirely. Mapping operating heritage to investment thesis is the highest-yield prospecting move available to a fundraising team.

5. The liquidity wave will reset commitment capacity in the second half

The SpaceX listing and Anthropic's IPO runway will convert large blocks of pre-IPO family-office paper into realized capital across Q3 and Q4. Combined with higher-for-longer rates that favor note-funded acquisitions and private credit, the families that participated in those cap tables will be the most active new LPs of the back half. The intelligence advantage is knowing who holds the exposure before the settlement dates.

6. Count beats dollars, and the offices that act on continuously refreshed signal win the allocation

May's $79 billion headline was one round. The families that wrote the other 50-plus checks did so across robotics, mRNA, ocean compute, marine concrete, women's sports and media control, most of which required same-week evaluation. By the time these deals appear in a quarterly database, the allocation windows have closed. The structural advantage belongs to offices and managers operating on live signal, not quarterly refreshes.

Altss lens: where the warm paths actually sit

The ICONIQ node. ICONIQ co-led Anthropic and continued in Primer in the same month, on top of a 2025 vintage spanning PE, credit, real assets, secondaries and GP stakes. If you are raising any alternative-asset vehicle, ICONIQ is the densest single family-capital aggregator to map, and the work is identifying which internal vehicle is the right door. Altss tracks ICONIQ's disclosed positions and fund filings so your outreach targets the specific strategy, not the brand.

The athlete-and-sports-principal cluster. Bolt Ventures (David Blitzer) appeared in both PlayerData and Just Women's Sports, and 35V (Kevin Durant) sat alongside Bolt in PlayerData and has prior positions across leagues and women's sports. Apollo Sports Capital and Dundon Capital anchor the pickleball platform, and Michael Dell sits in the Raiders group alongside Blackstone's Joseph Baratta. These overlapping cap tables form a navigable sports-capital graph: board seats and co-investor relationships from these deals are the warm-introduction paths into athlete-founded and sports-principal offices, which almost never respond to cold outreach.

The operating-family frontier-AI cluster. The Yamauchi No.10 office (Nintendo), Illusian (Supercell's Paananen) and the Thiel and Doerr principal vehicles all surfaced in the month's frontier AI and compute rounds. These are small, often non-Western, operating-heritage offices that sit on cap tables next to NVIDIA and Radical. Altss surfaces these offices by sector and operating origin, which is how you reach them through a referral one or two degrees out rather than a cold email a database would never even point you to.

The blue-economy and impact cluster. Builders Vision (Walton), now operating under a consolidated CIO with nearly 30 investors, traveled with Burnt Island Ventures and the Prince Albert II of Monaco Foundation's ReOcean Fund across CREW Carbon and ECOncrete. For climate and ocean managers, that recurring syndicate is a discoverable warm-path map into impact-anchored family capital that leads and anchors rather than co-invests concessionally.

Lead-capable versus participant offices. The single most actionable cut from May: Breyer, ICONIQ, Builders Vision and Premji can price and lead rounds, while Alpha Square (Corgi) and ICONIQ-in-Primer are participating in rounds others led. Pitch the lead-capable offices for anchor commitments and the participants for fill. Altss tags family offices by their demonstrated role (lead, co-lead, participant) per round, so your target list reflects what each office can actually do rather than where its name appears.

The liquidity tracker. SpaceX, xAI and Anthropic exposure is about to become the most valuable cap-table data in the market, because the families holding it are the most likely new LPs of the second half. Altss tracks pre-IPO family-office positions and surfaces them against the listing and settlement calendar, so your outreach reaches these offices inside the post-liquidity window rather than after it closes.

What remains unconfirmed: corrections and caveats

ICONIQ in Anduril and Sierra. Some trackers attribute ICONIQ or other family-office participation to Anduril's $5 billion and Sierra's $950 million rounds. Primary disclosure for those rounds names Thrive and Andreessen Horowitz (Anduril) and Tiger Global and GV (Sierra), and does not confirm a family-office position. We have excluded those attributions pending primary confirmation.

ECOncrete round size and lead. Builders Vision, Barclays Climate Ventures and the Prince Albert II of Monaco Foundation's ReOcean Fund are confirmed participants in ECOncrete's fundraise via the company's own disclosure, but the exact round size and lead investor are not independently confirmed, so we describe it as a fundraise rather than assigning a specific figure or lead.

Just Women's Sports round size. Bolt Ventures' late-May investment in Just Women's Sports is confirmed, but the round size was not disclosed in a primary release, so we report the participation without a dollar figure.

Census completeness. Altss tracked about 53 family-office direct investments in May, of which roughly 18 are publicly named in primary sources; the rest are confirmed through proprietary and primary-source collection. Public reporting structurally undercounts family-office activity, which is the coverage gap this series exists to close. Directionally, May held steady against April's 55 and well above March's 39.

Primer valuation. Primer did not disclose a post-money valuation for its $100 million Series C, so none is reported here.

FAQ

How many family-office deals closed in May 2026?

About 53 direct family-office investments tracked by Altss for May 2026, broadly flat against the 55 in April and well above March's 39. The count held steady even as disclosed value spiked, which is the central point: the dollar jump was concentration, not breadth.

Why was disclosed value so much higher than April if deal count was flat?

Because one round dominated. Anthropic's $65 billion Series H is roughly 82% of the $79.44 billion total, and the top three transactions (Anthropic, Dubai Holding's $6.5 billion Emaar stake, Anduril's $5 billion) are about 96% of it. Strip the mega-rounds and the underlying cadence is steady, which is why Altss leads with count over dollars.

Which family offices were most active in May 2026?

By visibility and lead capacity: ICONIQ (co-lead in Anthropic, participant in Primer), Breyer Capital (lead in ParcelBio), Builders Vision (active in CREW Carbon and ECOncrete), and the sports-principal cluster (Dundon in pickleball, Blitzer's Bolt across PlayerData and Just Women's Sports, Michael Dell in the Raiders). By novelty: the Yamauchi No.10 Family Office (Nintendo) in Decart and Illusian (Supercell's Paananen) in CodeWords.

Which sector led family-office deal flow in May?

Information Technology, with 15 deals, taking the top spot back from healthcare, which had led for the first time in April. Frontier AI, defense, enterprise software and payments drove the sector.

What was the biggest theme outside AI?

Sports and entertainment. Family and principal capital tied to the Las Vegas Raiders, Pickleball Inc., PlayerData and Just Women's Sports marked a shift from trophy ownership toward sports infrastructure, athlete data and media.

How did May compare with April and March?

Deal count was steady against April (about 53 versus 55) and well above March (39). Disclosed value jumped to $79.44 billion from $2.86 billion in April, but almost entirely on Anthropic's $65 billion round. The mix changed too: IT retook the sector lead from healthcare, and sports broke out as the clearest non-AI theme. The distortion is the same one March showed with OpenAI's $122 billion round.

Are sovereign and ruling-family deals counted the same way as venture rounds?

They are counted but quarantined. Dubai Holding's $6.5 billion Emaar stake is sovereign-adjacent ruling-family capital and an intra-government transfer, so we include it in the count but call it out separately so it does not distort the underlying venture and growth cadence. The same applies to control and M&A transactions like the Raiders and BuzzFeed.

Which family offices are investing in AI and AI infrastructure?

In May, confirmed: ICONIQ (Anthropic co-lead, Primer participant), the Yamauchi No.10 Family Office (Decart), Illusian / Ilkka Paananen (CodeWords), and the principal tier of Peter Thiel and John Doerr (Panthalassa). The notable shift is toward the infrastructure and energy layer (Decart's world models, Panthalassa's wave-powered compute) rather than only the model layer.

How will the SpaceX and Anthropic IPOs affect family-office allocations?

Family offices holding SpaceX, xAI or pre-IPO Anthropic exposure are positioned to convert large unrealized gains into realized capital across the second half of 2026. Historically, the 90 days after a major tech IPO are the highest-conversion window for LP commitments from offices that held the pre-IPO position. Tracking which offices hold that exposure ahead of the settlement dates is a concrete prospecting edge.

How can I track family-office deal flow in continuously refreshed?

Static databases refresh quarterly, by which point mandates have shifted and allocation windows have closed. Altss provides continuously refreshed LP intelligence across more than 9,000 verified family offices, with signal detection, relationship mapping, and verified decision-maker contacts, surfacing which offices are active now, what they actually invest in, and whether there is a credible warm path to a conversation.

Methodology

Altss counts a direct investment when a single-family office, multi-family office, principal investment group, founder-family vehicle, or sovereign-adjacent family vehicle appears on a company's cap table or transaction disclosure for that round. Each family office is counted once per round, and follow-ons are counted separately. Rounds with undisclosed value are included in counts but excluded from value totals. Mega-rounds, control deals and M&A (Anthropic, Emaar, the Raiders, BuzzFeed) are counted but called out separately so month-over-month value comparisons are not distorted. Deal facts in this review are drawn from company announcements, SEC filings, and primary news reporting, not from legacy fund-of-funds databases. See the full methodology for source rules and coverage caveats.

How Altss helps you track this deal flow

May is a clean illustration of why LP intelligence has to be built from the bottom up rather than inferred from registries or conference lists. The ICONIQ co-lead tier in a near-trillion-dollar AI round, the Nintendo and Supercell family offices on frontier AI cap tables, Michael Dell inside an NFL ownership group, Blitzer's and Durant's vehicles across athlete data and women's sports, Breyer leading a deep-science seed, Builders Vision anchoring ocean infrastructure, two principal-family media takeovers, and a record IPO about to reset commitment capacity all live in the messy overlap between venture, growth equity, real assets, control M&A and sovereign-adjacent capital. Almost none of it surfaces in a traditional workflow in time to act.

Altss maps more than 9,000 family offices and tens of thousands of institutional LPs, tracking not only stated mandates but actual allocations into AI, robotics, sports, media, climate, biotech and real assets, and tagging each office by its demonstrated role per round. If you are a GP raising a new fund, an IR leader building a co-invest program, or a family-office CIO benchmarking against peers, Altss gives you continuously refreshed, verified visibility into where these families are truly deploying, not just where their names appear on an agenda.

You can explore the full map of institutional capital flows and family-office deal flow at altss.com.

Find the allocators who actually back funds like yours

GPs and IR teams use Altss to surface verified LP decision-makers, recent mandate activity, and the warm paths into each — then prioritize outreach.

See the allocators behind your next close.

OSINT-native coverage of 9,000+ family offices and 30,000+ institutional investors, with verified decision-makers and a sub-30-day verification cycle.